Recourse vs. Non-Recourse Factoring — Who Eats the Loss If the Broker Doesn’t Pay?

What is the difference between recourse and non-recourse factoring?

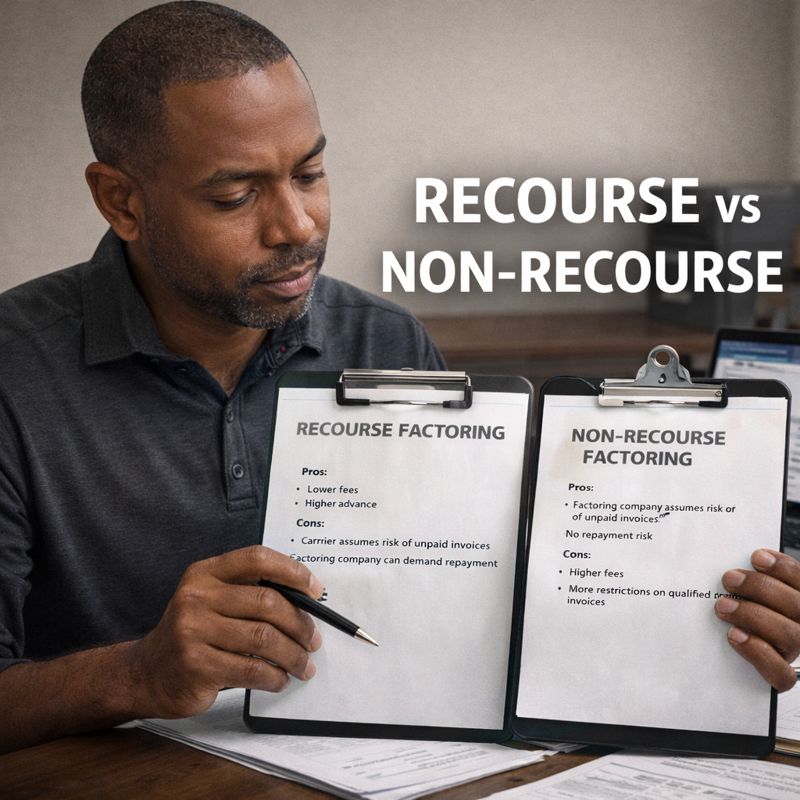

The difference between recourse and non-recourse factoring comes down to one key question: who is responsible if the broker or shipper doesn’t pay?

Owner-operators comparing factoring companies for trucking often reach this point when they’re close to signing and want to understand how much risk they’re actually taking on.

How recourse factoring works

With recourse factoring, the carrier may be required to repurchase an invoice if the broker fails to pay within a defined period. That responsibility is spelled out in the factoring agreement.

Recourse programs often come with lower fees because the factoring company is taking on less risk. For some operators working with well-vetted brokers, that tradeoff can make sense.

How non-recourse factoring works

Non-recourse factoring shifts certain types of non-payment risk away from the carrier. In many agreements, this protection applies specifically to broker insolvency or bankruptcy — not every possible reason a broker might delay payment.

Drivers searching for non-recourse factoring companies are usually trying to protect themselves from catastrophic broker failure, not routine paperwork issues.

What non-recourse does NOT mean

Non-recourse does not mean zero risk. Most agreements still require clean paperwork, proper delivery, and transactions that are free from disputes.

If a broker delays payment due to missing documents, claims, or load disputes, those situations may fall outside non-recourse coverage depending on the contract.

Why this decision matters

Operators comparing trucking factoring services are usually weighing two tradeoffs:

- Lower fees with more carrier responsibility (recourse)

- More protection with defined coverage (non-recourse)

Neither option is automatically better. The right choice depends on your broker mix, risk tolerance, and how much uncertainty your business can absorb.

Questions to ask before you sign

- What exact non-payment events are covered?

- How long before an invoice is considered unpaid?

- What documentation is required to maintain coverage?

- Under what conditions can an invoice be charged back?

These are the same questions experienced operators ask before submitting a trucking factoring application.

How Outgo fits the risk discussion

Outgo indicates that its factoring structure is designed to balance protection and flexibility, allowing carriers to manage risk without being locked into long-term commitments or forced usage.

Read what other truckers are reading

- What Is Factoring in Trucking — And When Should an Owner-Operator Use It?

- The Real Cost of Factoring — What Drivers Miss in the “Fast Pay” Pitch

- Factoring Contract Traps — Automatic Renewal, Exit Fees, and the Fine Print

- Factoring Alternatives — How to Improve Cash Flow Without Paying Fees on Every Load